You are about to leave the website of SDM Inc. ("SDM") and will be redirected to the website of SDM Financial Inc. ("SDM Financial"), a US affiliate of SDM providing crypto derivatives trading services.

Please be aware that SDM Financial's services are not intended for, and should not be used by, residents of Canada.

By clicking on the link to SDM Financial's website, you acknowledge and agree that: You are not a Canadian resident.

SDM Financial is not registered with any regulatory authority in Canada and is strictly prohibited from entering, or otherwise engaging in, any transactions with Canadian residents.

Non-Canadian residents who deal with SDM Financial do so at their own risk, and SDM will not be held liable for any losses or damages incurred as a result.

By clicking 'I Accept' below, you confirm that you have read, understand, and agree to the above . If you do not agree, please select 'I Decline' and you will be redirected back to SDM's website.

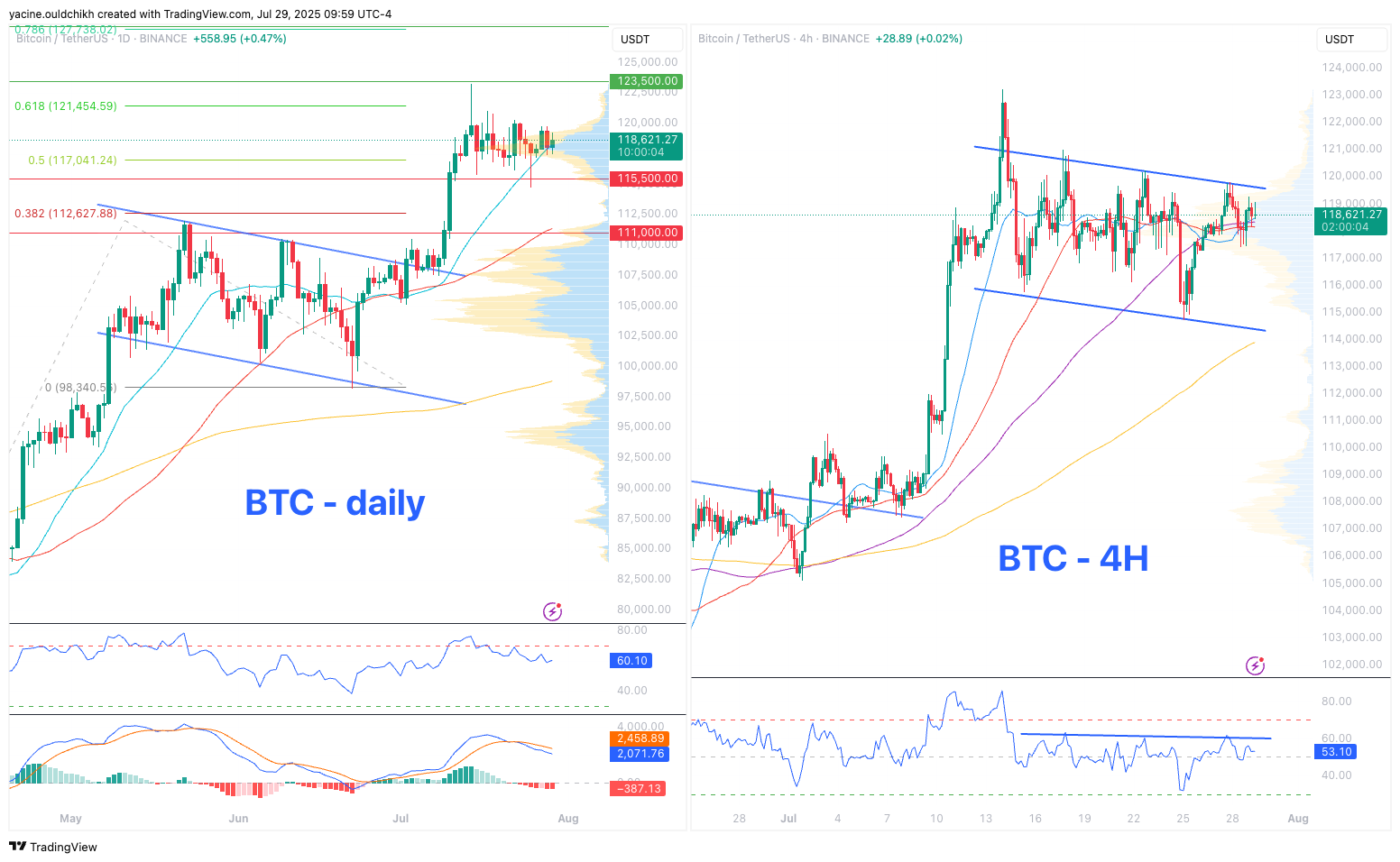

In a largely stagnant BTC market, the reactivation of long-dormant whale wallets has sparked concerns over possible profit-taking by early investors. Meanwhile, any hopes of an altcoin season seem to have faded, with BTC’s annualized funding rate sitting at 10%, notably higher than most major alts. On the options front, sentiment is mixed: Deribit BTC risk reversals are tilting bearish with a front-end put skew, while ETH risk reversals remain biased to the upside across the curve.

BTC is testing support at its 20-day moving average, and a decisive break lower could open the door to downside targets at $116,500 and $115,500. On the flip side, ETH has been gaining ground, driven by a surge in institutional participation, corporate treasuries now account for 1% of ETH’s total supply. The ETH/BTC ratio has jumped from 0.018 in April to 0.033 in July, bolstered by both ETF inflows and treasury buying.

In a notable shift, Ray Dalio is now recommending a 15% portfolio allocation to Bitcoin or gold, up from his previous 1–2% stance, citing growing concerns over U.S. fiscal imbalances and long-term currency debasement. While Dalio still favors gold over BTC due to blockchain transparency concerns, he emphasized that the split between the two can be flexible.

Elsewhere, markets shrugged off the U.S.–EU trade deal, but attention is turning to potential U.S.–China negotiations ahead of Friday’s tariff deadline. Any progress there could be a market mover.

The News Room

BlackRock’s ETHA becomes 4th‑largest ETF by 30‑day inflows as Ethereum funds aim for $10 B

BlackRock’s iShares Ethereum ETF (ETHA) has surged to the fourth-highest ranked ETF by 30-day inflows, capturing roughly $9.34 billion in July—around 91% of all inflows into spot Ethereum ETFs, and nearly four times more than Fidelity’s FETH. The broader category amassed $9.3 billion through July 25, up 120% from the month’s start, with a daily average of ~$233 million—putting ETHA on track to hit $10 billion in inflows by month-end. Its trading volume of $1.35 billion on July 28 places it among the top 0.4% of all ETFs, underscoring institutional investors’ accelerating interest in ETH exposure.

Interactive Brokers weighs launching customer stablecoin to power 24/7 funding

Interactive Brokers, a ~$110 billion discount brokerage, is exploring issuing its own stablecoin to facilitate around-the-clock funding and crypto transfers for client accounts. Founder Thomas Peterffy frames the exploration cautiously—though open to adoption if value becomes clear—and says decisions about structure and rollout remain pending. The firm may also offer third-party stablecoin support, depending on issuer credibility, as it deepens its crypto infrastructure alongside partnerships with Paxos and Zero Hash.

Global stablecoin searches hit all‑time high with Washington leading traffic

Search interest in stablecoins has reached a new global peak in July 2025, coinciding with the U.S. GENIUS Act’s enactment, which established the country’s first federal regulatory framework for payment stablecoins. The spike was most pronounced in Washington, D.C., followed by nearby Hyattsville and Arlington, suggesting rising market and legislative focus. Search volumes outpaced previous highs seen during the EU’s MiCA rollout, reflecting growing mainstream curiosity around stablecoins’ role in digital finance.

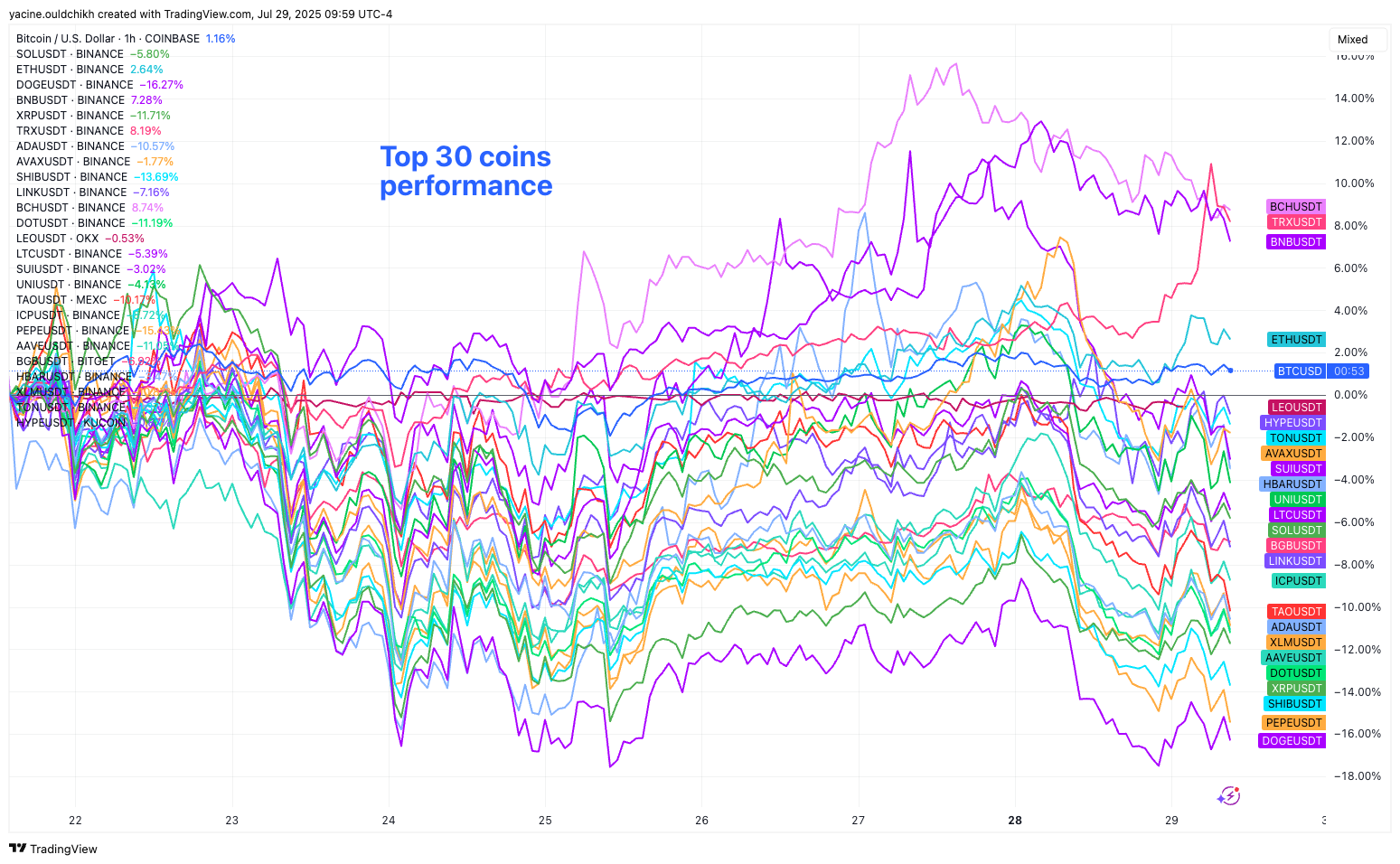

Crypto Charts

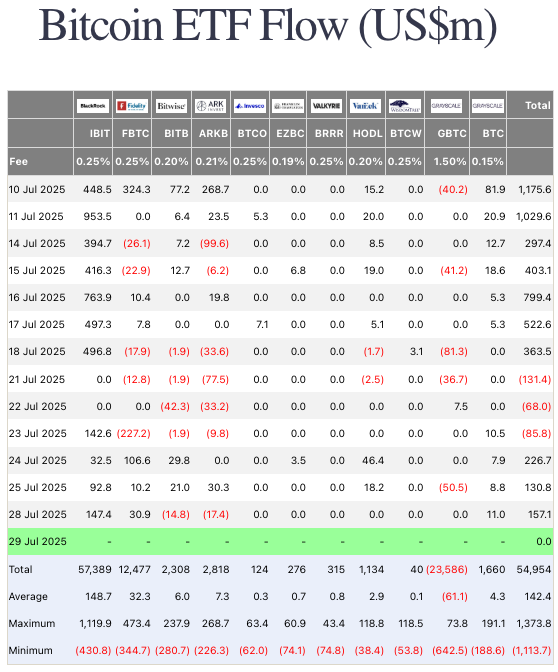

ETF Flow

Disclaimer

This research is for informational use only. This is not investment advice. Other than disclosures relating to Secure Digital Markets this research is based on current public information that we consider reliable, but we do not represent it is accurate or complete, and it should not be relied on as such. The information, opinions, estimates, and forecasts contained herein are as of the date hereof and are subject to change without prior notification. We seek to update our research as appropriate.

Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. The price of crypto assets may rise or fall because of changes in the broad market or changes in a company's financial condition, sometimes rapidly or unpredictably. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Fluctuations in exchange rates could have adverse effects on the value or price of, or income derived from, certain investments. We and our affiliates, officers, directors, and employees, excluding equity and credit analysts, will from time to time have long or short positions in, act as principal in, and buy or sell, the securities or derivatives, if any, referred to in this research.

The information on which the analysis is based has been obtained from sources believed to be reliable such as, for example, the company’s financial statements filed with a regulator, company website, company white paper, pitchbook and any other sources. While Secure Digital Markets has obtained data, statistics, and information from sources it believes to be reliable, it does not perform an audit or seek independent verification of any of the data, statistics, and information it receives.

Unless otherwise provided in a separate agreement, Secure Digital Markets does not represent that the report contents meet all of the presentation and/or disclosure standards applicable in the jurisdiction the recipient is located. Secure Digital Markets and their officers, directors and employees shall not be responsible or liable for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses, or opinions within the report.

Crypto and/or digital currencies involve substantial risk, are speculative in nature and may not perform as expected. Many digital currency platforms are not subject to regulatory supervision, unlike regulated exchanges. Some platforms may commingle customer assets in shared accounts and provide inadequate custody, which may affect whether or how investors can withdraw their currency and/or subject them to money laundering. Digital currencies may be vulnerable to hacks and cyber fraud as well as significant volatility and price swings.

Contact Us

Sign up to receive more exclusive market coverage: